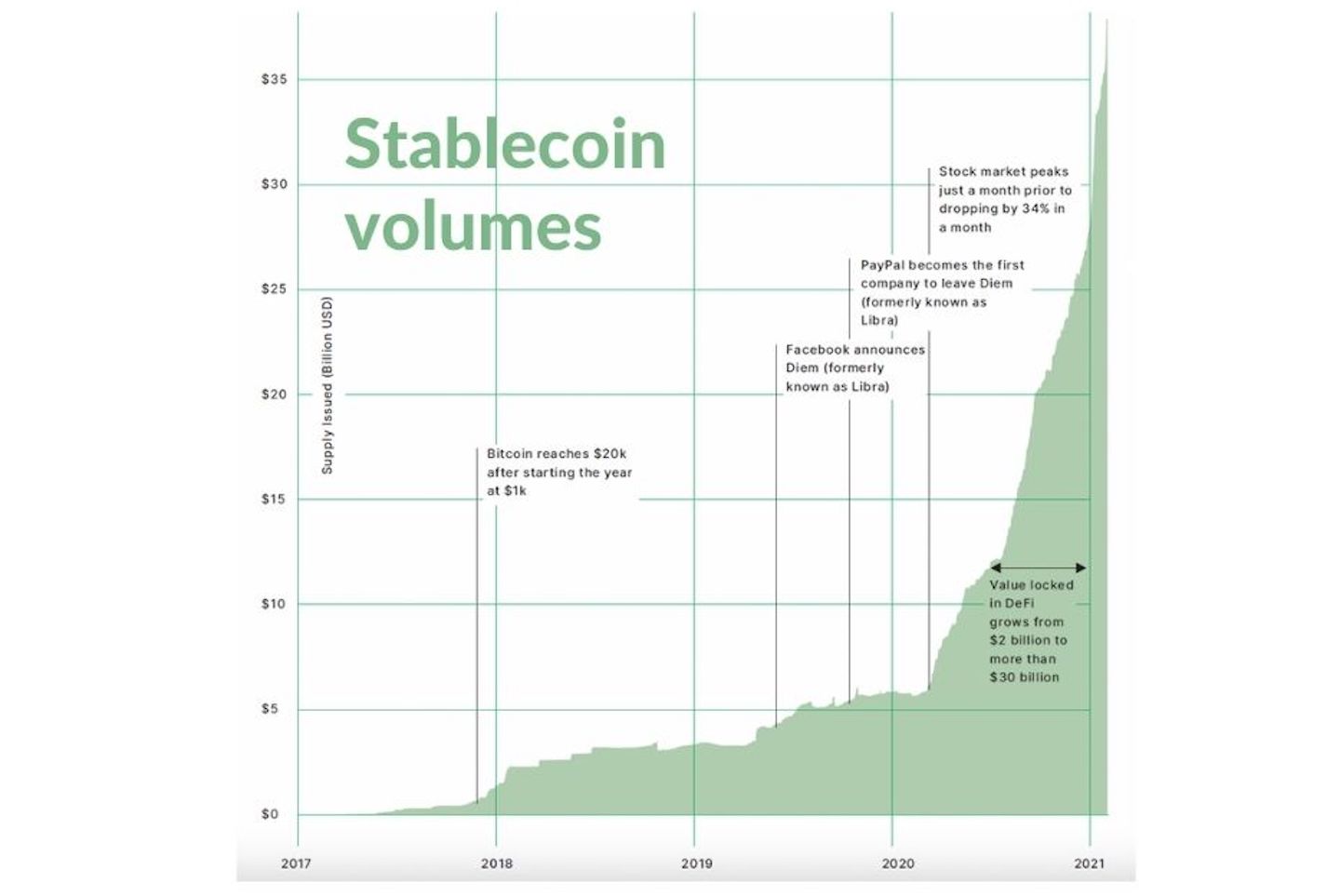

The stablecoin universe has reached nearly $40 billion in supply and, in January 2021, monthly transaction volume exceeded $200 billion.

For all the headlines commanded by Bitcoin, the real story in cryptocurrency may be stablecoins, which present the best opportunity to allow digital assets to scale into everyday financial services.

Stablecoins are emerging as the private sector’s answer to central-bank digital currencies, with the likes of PayPal, Facebook-backed Diem, and crypto-native stablecoins poised to use these tools to transform payments and other financial services.

Instead of a Big Bang, however, the transition is likely to be gradual. There are plenty of frictions, not least incoming regulation, which could either boost the industry or crimp its prospects.

Origins and uses

A newly released research report by U.S. media and consultancy The Block offers a comprehensive view of the fast-emerging sector, explaining how it could leap out of its crypto niche and have a much wider impact – as well as the regulatory and market impediments it must overcome.

Stablecoin issuers got their start targeting crypto enthusiasts and traders, but they are now looking at payments, remittances, and serving as gateways in and out of crypto for banks, asset managers, and other financial institutions.

Stablecoins are digital representations of fiat currency that live on blockchains. The paper says some market participants liken them to Eurodollars. These “cryptodollars” are cryptographic tokens which circulate on public blockchains and aim to track the return of sovereign currencies. Most of them are redeemable for actual dollars in bank accounts, making them essentially bearer assets, in digital form.

The first stablecoins emerged in 2014 and 2015 as a response to the high volatility of Bitcoin, Ethereum and other cryptocurrencies, which needed a stabilizer to make it possible to use them as means of transferring money within the crypto world. To date, Ethereum’s blockchain has been the preferred choice on which to launch stablecoins.

Unregulated exchanges that lack access to fiat banking, such as Binance, Huobi and OKEx, have found these invaluable “on ramps” to onboard retail participants and ramp up their own deposit bases of fiat currency.

Designs

At their heart, stablecoins are meant to be stable relative to a benchmark (regardless of the volatility of the underlying asset). Their designs, however, vary.

The most common is the fiat-collateralized stablecoin, issued by a third party and backed by a single fiat currency, cash equivalents, or a basket of multiple fiat currencies.

Tether is by far the biggest stablecoin in circulation, and it is supposedly backed by a vault of U.S. dollars. Others in this vein (and with more credibility) include USDC and Paxos. Diem (formerly known as Libra) may launch this year as a combination, with a multi-currency coin and a series of single-currency versions.

Another type of stablecoin is one that relies on crypto assets for collateral, rather than fiat, although they are “soft pegged” to a fiat base. Given the untested nature of these projects, the market demands they be over-collateralized. It’s basically a tokenized IOU.

The crypto-asset overcollateralized stablecoins are more decentralized, which has its appeal in the world of DeFi, or decentralized finance. But they are harder to scale because growth depends on demand for using them as loans.

The third type of stablecoin is the algorithmic or non-collateralized stablecoin. These have a flexible supply that is governed by software to incentivize market players to buy or sell, in order to maintain price stability against the underlying currency. This requires a double- or even triple-layer of tokens, one a utility token representing the network and its governance, and others representing shares or bonds that are issued or burned to maintain market levels.

The complexity of algo stablecoins, and the risk that regulators deem some of their tokens to be securities, has prevented a big success story from this quarter. The largest is Dai, which accounts for 4.3% of total stablecoin issuance, but it is the most volatile of leading stablecoins.

Tether

Although the stablecoin world comes with a lot of variety, by far and away the main narrative is around Tether. There are about 50 different live stablecoins, issued by 25 companies, with total supply of $38.5 billion. Of this, 99.5% is pegged to the U.S. dollar, and 70% of the total consists of Tether, or USDT. Its nearest competitor is USDC, also tied to the dollar, and although USDC is widely considered more credible (as in, it actually has the dollars in reserve it claims to have), it is only 15.8% of stablecoin value outstanding.

The Block’s report says, “Tether is unmatched when it comes to trade volume on centralized exchanges.” In January 2021, it saw $495 billion of volume. This is partly because Tether enjoys a network effect: people use it because people use it. Unlike USDC and other rivals, Tether is also not associated with the United States, so it is used by people outside of U.S. jurisdiction who want exposure to the U.S. dollar – hence its popularity on Asian crypto exchanges, and its acting like a digital Eurodollar.

Although Tether is keen to expand into micropayments or other uses, it’s main raison d’être is for traders who need a stablecoin to move money across exchanges, switch into fiat, or use as collateral for futures positions.

Tether has been printing coins at a furious rate as the value of Bitcoin has skyrocketed. The Block report explains that most Bitcoin miners are in China, and they pay for their operating expenses (electricity, etc.) in Tether by borrowing it against the Bitcoin they are creating.

Tether issuance got its first big bump in March 2020 when Bitcoin’s price crashed in line with all other risk assets, in the great COVID-19 selloff. That destroyed the value of miners’ Bitcoin collateral, so they began buying Tether instead.

This also had a knock-on effect in the world of derivatives exchanges. BitMEX, then the leader in crypto derivatives, insisted on bitcoin as collateral for its perpetual swaps and futures. Other exchanges allowed U.S. dollar collateral – include dollars expressed as Tether. BitMEX, amid power outages and later allegations by the U.S. government of laundering money, has seen Tether-fueled competitors totally outpace it since.

The rise of U.S. dollar collateral on venues like Binance, Huobi and OKEx have made Tether, not Bitcoin, the biggest player in crypto trading. Today 60% of all volume is denominated in Tether and another 4% in other stablecoins, according to The Block’s research. Only about 11% comes from Bitcoin pairs.

Tether is also controversial. Its backers are tied to a crypto exchange, Bitfinix, and have been found by the U.S. Department of Justice to have lied about their dollar holdings, which the company has always sought to keep opaque. The company recently settled out of court. Market players have told DigFin that reliance on Tether is “dangerous” but demand remains robust. The Block’s report alluded to these developments obliquely, suggesting readers “do their own research”.

Other stablecoins

Other stablecoins are likely to win market share as their use cases become more relevant. USDC is already preferred for small-value transactions. A Korean stablecoin, TerraKRW, shows promise as an algorithmic stablecoin for local merchants – it is struggling to scale outside of Korea, especially as it would be going up against e-wallets run by the likes of WeChat Pay and LINE. But it could set an example for other local coins.

The growth of decentralized finance, or DeFi, has also boosted the use of stablecoins. The DeFi world’s total value passed $30 billion in January, versus only $1 billion about 18 months ago. Stablecoins help with lending and non-custodial trading, and as DeFi applications expand, there will be new demands for stablecoins.

Finally, if Diem, PayPal or others launch their stablecoins this year, this will provide the market with a huge boost, as well as create new products. These may not rival Tether in the trading space but could become important bridges between the traditional world of finance and crypto, and make possible payments, cross-border settlement, credit, and other services in digital form – particularly if they are able to interact with public forms of money, that is, CBDCs.

Regulation

This rosy outlook will rely on appropriate regulation. Governments are taking different approaches to stablecoins. The Block’s report goes into detail on some of these initiatives in the U.S. and Europe. In both cases, authorities tend to regard stablecoins as extensions of traditional payments. They see value in stablecoins’ ability to serve as a store of value and as a means of payment – two classic definitions of money.

But authorities do not seem to regard stablecoins as units of account. This is the third classic role of money. This approach is probably deliberate, as governments will continue to guard the primacy of sovereign fiat currency as the arbiter of prices. That vision will hold true so long as stablecoins are used as on-ramps into crypto. It seems less relevant to crypto-native projects, such as in the DeFi space.

Governments are not in agreement on how to manage the rise of stablecoins and crypto in general. They are justifiably concerned about crypto evading reasonable protections, such as anti-money laundering rules.

Within the United States, some regulators such as the Office of the Comptroller of the Currency, have staked out progressive, pro-stablecoin views.

Other authorities and politicians want to impose banking regulations on the industry – usually in the cause of protecting investors and their data, although The Block report noted the possibility that some government actors want to protect banks.

Both Washington and Brussels could pass laws that limit innovation in digital payments and stores of value in their jurisdictions. Taken to an extreme, some proposed legislation might threaten the underlying blockchain protocols themselves, such as Ethereum, upon which most stablecoins operate.

But regulators could also help stablecoins realize their potential, as mechanisms for transmitting, storing and settling value using distributed-ledger infrastructure. In this view, blockchains are regarded as the rails for the Internet of Value, just as networks such as SWIFT were for the technologies of the twentieth century. Regulators who support this level of innovation can bring clarity and assurance to the crypto world, and position their mar